FF Life: How much should you invest in a stock?

Percentage returns are irrelevant if the invested amount was small to begin with. There's an optimal amount that could bring meaningful gains to your total wealth, while limiting loss

26 May 2023· 4 min read

TL;DR

Business leaders often fixate on impressive percentage returns, yet this article argues these are 'vanity metrics' if the initial investment is trivial. True wealth creation hinges on absolute returns, underscoring the critical importance of strategic 'position sizing' – how much capital to deploy. A 1000% return on a tiny investment is negligible; a 50% return on a significant position can be transformative. The core insight: consciously determine optimal investment amounts for meaningful absolute gains, rather than chasing high percentages on inconsequential sums. This approach, coupled with intelligent diversification for capital preservation, empowers leaders to make strategic investment decisions that genuinely impact overall wealth and business longevity.

This was a few years back. I was an early investor in a startup, which had raised a round of funding from a VC investor. I was making many dozen times my initial investment.

Fantastic! I first thought.

But my life did not change much. In fact, I was mildly annoyed by the whole situation.

Now, don't think that I am ungrateful. It was just that the amount I had invested in the first place was so small that the resulting wealth was not life-changing by any means.

Oops!

Percentage returns vs absolute returns

In real life, when it comes to creating wealth, it is the absolute amount of money that we have and the absolute returns that we make that are of consequence.

Absolute Returns = Return % X Amount invested

In this formula, we tend to be fixated on the return percentage and we hardly ever talk about the right amount of investment.

In some ways, that’s understandable, as people are discreet about revealing their actual wealth — social norms dictate that you never ask someone how much they earn. We tend to abstract absolute amounts when conversing with each other. Percentages come in handy.

I argue that returns percentages and internal rate of return (IRR) are just a vanity metric. Because you cannot pay for coffee using IRR!

When a friend tells us, “I just bought a stock that has doubled for me”, before feeling a rush of envy, we need to ask ourselves whether this enterprise has made any significant wealth for them. Is it the case that they invested all their money and doubled it? Or was it $100 in and $200 out?

There are many ways to make the same amount of wealth

When making a new investment, the investor can decide to invest any fraction of their wealth. In market lingo, an investment is a position, and the size of the investment is the position size. Determining how much to invest is hence position sizing.

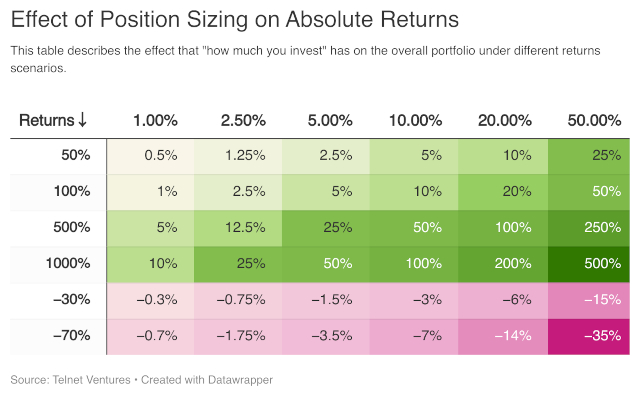

Notice that you can add 10% to your wealth in many ways:

- Invest 1% of the portfolio and the investment makes 1,000% returns

- Invest 10% of the portfolio and the investment makes 100% returns

- Invest 20% of the portfolio and the investment makes 50% returns

Maximum position size versus diversification

Let us first get the obvious out of the way: investing the entire portfolio in one or two risky investments is simply foolish. The possible gains from such an enterprise may be stupendous, but so can be the losses (see the last column in the table above).

Bear in mind that it is capital that forms the raw material of investing, and once it is lost (or significantly depleted) the investor can be set back many years.

It is precisely for this reason that individual investors with capital must avoid large losses like the plague, even if it means that their returns are mediocre (a topic we discuss in more detail elsewhere).

Diversifying the portfolio ensures that the investor prioritises survival over investment returns.

A typical diversified portfolio will hold multiple types of assets and investments. The largest single position in the portfolio can be 10-30% depending upon the risk profile of the investor.

Lest this may sound overly conservative, note that all professional fund managers are constrained by regulations, or their own charter, to limit their largest position at, say, 10% of portfolio; exposure to an industry sector or business group at 30% and so on. These position limits eliminate the risk of the fund blowing up.

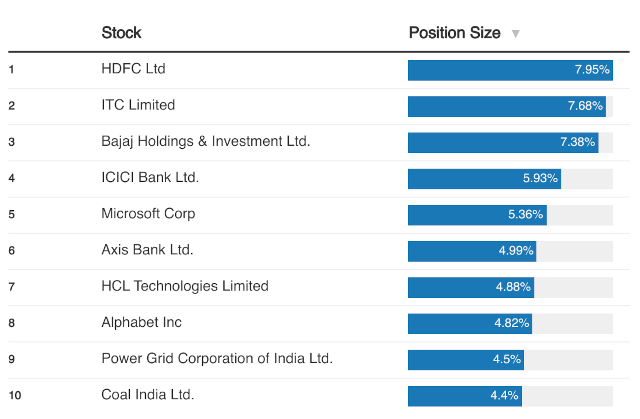

As an example, see the top holdings of Parag Parikh Flexi Cap Fund, a reputed mutual fund:

Is there a minimum position size?

Now, we come to the key insight of this piece. What is not very intuitive is that there must be a minimum ticket size for all positions, as I painfully learned from my startup investing experience. (In my defence, I had proposed to invest a decent amount, but because of oversubscription, it was whittled to a small cheque. It still causes me consternation, since large winners are so rare and I have wasted one of them already!)

What determines this minimum size? The minimum investment size should be such that if the investment goes up in percentage terms, the actual monetary gains ought to be at a meaningful level of the overall wealth.

1% of the portfolio must be the absolutely minimum position size for most people. In fact, I will recommend a higher number of around 2.5% for those that manage an active portfolio.

This means that an investor with a portfolio of $100,000 has no business investing $100 in any asset. Because no amount of returns will make the exercise meaningful in the bigger picture.

Added advantage: Limited number of positions. As a result of stipulating a minimum position size, the number of investments that an investor will hold at a time would be between 20 and 30 and not in hundreds. This affords some key benefits.

Firstly, a set of 20-30 companies is practical to analyse, track and to stay on top of, instead of hundreds of investments (most of which will be inconsequential).

Secondly, the investor can no longer make lazy decisions of investing insignificant amounts of money into every tip they receive from friends or from business news. Every new investment decision will now require significant thought because a decent amount is involved.

How to arrive at the right size for a position?

If just the thought of the future loss of an investment is freaking you out, you are over-investing.

On the other hand, if thinking of a potential loss on an investment is not making you too concerned, you are most likely under-investing. “Oh, I just invested $500 into this stock. It’s nothing.”

The correct size of a position is at which there still exists a healthy fear of loss. Only if the imagined losses from a position feel material will the possible gains be meaningful too.

What kind of candidates qualify for the maximum position size?

Let’s consider a potential investment where the possibility of losing money is very low. This happens rarely. It could be a stock trading below its intrinsic value, say, ITC or ICICI Bank in the last few years.

In these cases, the investor should not hesitate to invest 10-20% of their financial portfolio in a single position.

Assume that you invest 20% of your wealth into a value stock. “Even” if this stock were to go up 50% in a year or two, it earns 10% of incremental wealth to the portfolio.

To generate the same 10% of incremental wealth, a 1% position size would have to go up 10 times (1,000%)!

Which is an easier call? To find a stock that is likely to go up 50-100% in a couple of years, or one that is set to go up 10 times?

This is the prime advantage of value investing. When there is a limited downside risk, there is a greater margin of safety and hence the investor can bet the farm.

At a large position size, even a modest % return leads to significant wealth enhancement.

Position sizing plan for an individual long-term investor

- Prune the list of stocks in the portfolio. Get rid of all stocks that are less than 1% of portfolio

- A public markets portfolio construction as illustration. Remember that for most individuals Mutual Funds and ETFs are the best way to invest

- After any version of the above portfolio is fully deployed, a new stock can be added only by exiting an existing stock. This leads to automatic forced ranking.

- If a conviction stock triples and becomes 15% of the portfolio, do not do anything. Do not be eager to sell the winners. This is one big advantage that individual investors have over fund managers.

Join the conversation

Krishna Jha

Independent investor

Krishna is an independent investor managing a portfolio of both private and public companies.

He is an angel investor in a couple dozen startups while his public portfolio is focused on Indian companies with long-term holding periods.

In his previous avatar he was a technology entrepreneur and his first company was acquired by Infosys spin-off OnMobile.

Website: https://www.krishnajha.com/

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Loading comments...

Readers also liked

·FF Life

FF Life: How golf made me a better investor

The game is a good analogy for the markets and investing behaviour

KJ

Krishna Jha

Independent investor

FF Life: How golf made me a better investor

The game is a good analogy for the markets and investing behaviour

Independent investor

·FF Life

FF Life: Getting Hands-On with AI

Five curated stories on how and why to begin experimenting with AI

FF

Founding Fuel

FF Life: Getting Hands-On with AI

Five curated stories on how and why to begin experimenting with AI

·FF Life

FF Life: How to keep your fitness resolutions

A doctor and a trainer’s insights on what makes fitness a habit

CA

Charles Assisi

Co-founder and Director | Founding Fuel

FF Life: How to keep your fitness resolutions

A doctor and a trainer’s insights on what makes fitness a habit

Co-founder and Director | Founding Fuel

Explore more

Dive into other themes from our network.