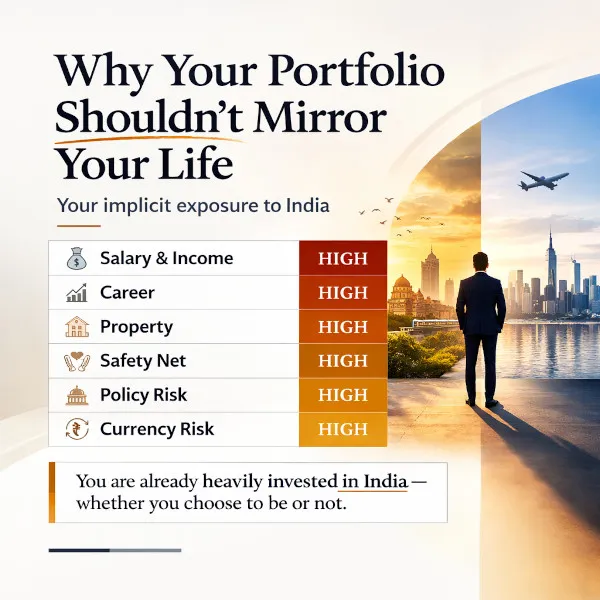

Most Indians don’t realise this, but if you earn in India, you are already massively long India. Your salary, employability, home equity (if you have it), social safety net, and political risk are all India-linked. When you then build an equity portfolio that is also overwhelmingly India-linked, you’re highly concentrated.

And concentration in investing is an unpriced risk.

It was October 2022. I was leading marketing at Kotak Cherry, surrounded by some of the smartest investment minds in Mumbai. A colleague—now a friend—told me this was the moment to “buy the Nasdaq.”

He didn’t mean buying a few US tech stocks because social media said so. He meant using the drawdown to start building global equity exposure. The Nasdaq had fallen sharply that year, and his reasoning was simple: it was a value opportunity.

The mechanics of investing abroad from India are no longer the hard part. Investing abroad used to be considered something that only the wealthy would do. It was news when an Indian billionaire bought a hotel in Great Britain. Today, investing abroad is normal. Boring even. Mutual funds, direct platforms, GIFT City—the routes exist. It is productised. The real challenge is building a clear rationale for why you’re doing it, and executing it in a way that won’t end with an anxious email to your CA in March.

Change the Way You View Diversification

Most of us think about diversification as a stock-market concept. It’s actually a life concept.

Your human capital and future earning potential are not diversified. They are concentrated in one economy, one currency, and one regulatory environment. So when people say, “I’m bullish on India,” what I hear is: “I want my investments to have the same risk factors as my life.”

That can work. It can also fail spectacularly, because you don’t get to rebalance your job the way you rebalance a portfolio.

The best argument for global investing isn’t higher returns. It’s risk governance: reducing the chance that one macro story—good or bad—defines your entire financial future.

What If You Are ‘Bullish on India’?

When people say “I’m bullish on India,” I understand the sentiment. But “bullish” is not an asset-allocation policy. Countries can be extraordinary and still deliver long periods of underwhelming equity outcomes—especially after bubbles, policy errors, or valuation peaks.

India can be doing well even as Indian equities disappoint.

Data from HDFC’s Yearbook 2026 illustrates this contrast.

On the macro side, India’s growth outlook remains structurally stronger than most large economies: projections show India at about 6.6% real GDP growth versus the world at roughly 3.2%, the US at 2.0%, and China at 4.8%.

On the market side, the same Yearbook notes that Indian markets have underperformed broader emerging markets significantly in certain periods, calling one such phase the worst underperformance in decades.

The global opportunity set is simply larger. Global equity market capitalisation is estimated at around $145 trillion—a scale far beyond any single country.

In CY 2025 (USD terms), different asset classes delivered very different outcomes: gold rose sharply, major US technology stocks performed strongly, several developed markets posted moderate gains, while some commodities and currencies lagged.

In short, economies and equity returns are related—but not married.

That’s why diversification is not a view on India—it’s a view on uncertainty.

Currency, Population, and Geopolitics

Once you invest abroad, you introduce currency into your return stream. If your future liabilities are partly foreign-currency linked—overseas education, travel, imported goods, global services, even healthcare—foreign assets can act as a partial hedge.

Since liberalisation in 1991, the Indian rupee has depreciated over the long term against the US dollar. While currency movements are never linear, long-term trends matter when planning multi-decade financial goals.

India’s demographic story is powerful, but population growth does not automatically translate into shareholder returns. That requires productivity gains, corporate profitability, capital-market depth, and sustained execution.

Geopolitical risk is another factor. It can reshape supply chains, tariffs, energy prices, and capital flows. Geographic diversification does not eliminate such risks, but it reduces dependence on any single geopolitical fault line.

History offers cautionary examples. Japan’s asset bubble peaked in 1989, after which the Nikkei took decades to revisit those levels. The Asian financial crisis of 1997 severely impacted several fast-growing economies. These episodes are not arguments against those countries; they are reminders that concentrating wealth in a single market can create long periods of stagnation.

Why Indian Investing Is the Default Setting

Before framing this as patriotism or excessive optimism, it’s worth noting that home-country bias is a global phenomenon. Investors everywhere prefer domestic assets.

In India, this bias has additional drivers.

One is familiarity. Most investors understand companies they encounter daily—banks, telecom firms, IT companies—far better than distant global firms.

Second is convenience. Domestic investing has been productised into one-click SIPs. Global investing still involves remittance rules, documentation, foreign statements, and perceived complexity.

Third is narrative. Investing in Indian equities often feels like investing in India’s future itself. The optimism may be justified, but optimism is not an allocation framework.

As one fund manager has pointed out, India accounts for only a small share of global market capitalisation. Concentrating most of one’s portfolio in a single country simply because one lives there ignores the scale of the global opportunity set.

A cleaner mental model is three buckets:

- US—large market, not the whole market

- Developed ex-US—Europe, Japan, etc.

- Emerging ex-India—broader EM opportunity set

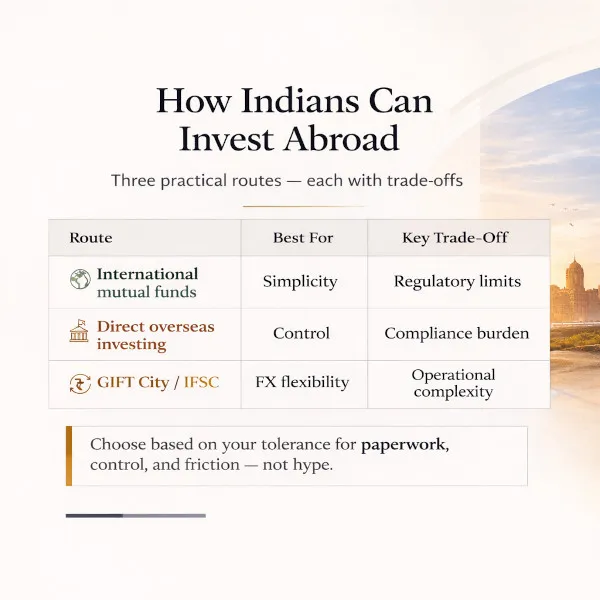

The How

There are three mainstream routes for a resident Indian to get overseas equity exposure. Each involves a different balance of simplicity, control, and administrative effort. The best choice depends less on expected returns and more on how much complexity you are prepared to manage. If you want to get into it, there’s a discussion guide at the end of this article to help you talk with your financial advisor.

Route A: India-Domiciled International Mutual Funds / FoFs

This is the “global exposure with domestic convenience” route. You invest in INR through familiar platforms, receive a NAV and statements, and handle taxes within the usual mutual-fund framework.

The main constraint is regulatory limits on how much Indian mutual funds can collectively invest overseas, which can temporarily restrict inflows. Many such funds also invest via underlying offshore vehicles, which can increase costs.

Tax treatment broadly follows mutual-fund rules, though investors should verify specifics for each scheme.

Route B: Direct Overseas Investing via Indian Platforms

Indian fintech platforms allow investors to buy foreign stocks or ETFs under the Liberalised Remittance Scheme (LRS), which permits remittances of up to USD 250,000 per financial year for permissible purposes. With some brokers, one can buy stocks at as little as $1.

This route offers maximum flexibility and direct ownership but requires attention to foreign exchange costs, tax reporting, and compliance obligations, including disclosure of foreign assets and income.

Budget changes have adjusted thresholds for tax collected at source on overseas remittances, so investors should confirm current rules before transferring funds.

Route C: GIFT City / IFSC Structures

GIFT City’s International Financial Services Centre provides access to foreign-currency investments within a special regulatory framework and may offer lower transaction frictions.

Investment options include foreign-currency accounts, securities traded on IFSC exchanges, pooled investment vehicles (fund houses like DSP and PPFAS have begun offering these, though there's an entry barrier: a minimum initial investment of $5,000), and certain global instruments. However, for Indian residents, income from these investments is still taxable in India as global income.

It is best viewed as a regulatory and operational alternative rather than a tax-free jurisdiction.

Across all routes, the principle is the same: understand the paperwork, maintain records, and consult qualified professionals when needed.

The Real Point

This is not an anti-India argument. It is a pro-resilience argument.

If your global allocation is zero, you are forced to be right about India every year. If your allocation is diversified, you can be wrong sometimes and still be financially secure.

You can believe deeply in India’s future and still recognise that your financial future should not depend on a single country.

You can love India—and still invest in the world.

Dig Deeper

Thinking of evaluating global investing more seriously? These resources can help you frame the right questions before taking action.

Why investing abroad matters for Indian investors—Saurabh Mukherjea, founder and chief investment officer, Marcellus Investment Managers

A clear practitioner’s perspective on currency risk, concentration, and the case for global diversification. (Play time: 21 mins)

Questions to discuss with your investment advisor before investing abroad

Link to your Gdoc companion

A structured checklist to evaluate tax, compliance, and suitability in your own situation.