Factories Without Formulas

India is investing billions in battery manufacturing. But without the capital to fund indigenous technology, the intelligence inside those factories may continue to be imported.

22 April 2026· 4 min read

TL;DR

India's multi-billion-dollar investment in battery gigafactories critically overlooks a foundational element: indigenous core technology. While manufacturing scale is aggressively funded, the intelligence powering these factories remains largely imported, creating an import-dependent energy transition, reminiscent of past challenges in solar.

A nascent, vibrant ecosystem of Indian battery tech startups is developing cutting-edge innovations, yet faces a formidable "valley of death." These ventures struggle to secure the crucial capital needed to scale from prototype to pilot production, compounded by lengthy OEM qualification cycles. True localisation and long-term competitive advantage demand not just manufacturing capacity, but strategic investment in domestic R&D and bridging the funding gap for technological innovators. Prioritising this will secure India's technological sovereignty in the global clean energy race.

India is building gigafactories. What it is not yet building is the technology that goes inside them.

Industrial groups like Reliance, Amara Raja, and Exide are committing billions to battery manufacturing. But each of them depends on foreign partners for cell chemistry. Alongside them, a smaller, quieter ecosystem of Indian startups is trying to build battery technology from scratch. They are not short on ambition. What they lack is the kind of capital that allows that ambition to survive long enough to matter.

This is the tension at the heart of India’s battery story: manufacturing scale is being funded. Technological risk is not.

India is building gigafactories. What it is not yet building is the technology that goes inside them.

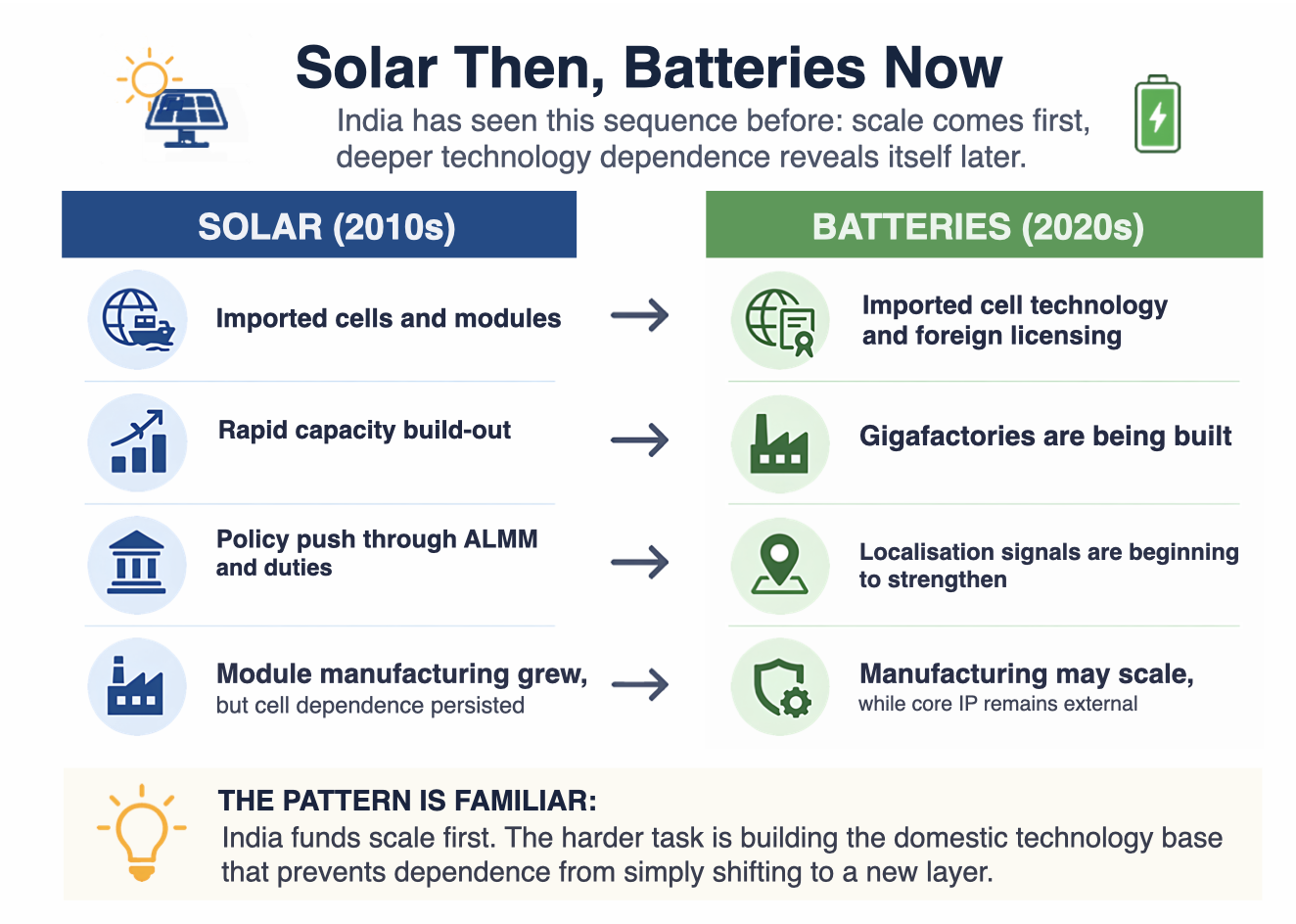

An import-dependent energy transition

India’s energy transition will run on batteries. Electric vehicles, renewable energy storage, and distributed power systems could push annual battery demand to 200 GWh by 2030—roughly ten times current levels. Today, over 90% of battery cells are imported, primarily from China, South Korea, and Japan.

Policy has responded with scale. The government’s Advanced Chemistry Cell (ACC) Production Linked Incentive scheme has committed ₹18,100 crore to build 50 GWh of domestic manufacturing capacity. Reliance and Ola Electric are setting up gigafactories under this scheme. Others, such as Amara Raja and Exide, are building capacity outside it.

But the underlying pattern remains unchanged: the factories may be domestic, the technology inside them is not.

This is not unfamiliar terrain. Solar followed a similar trajectory. India scaled capacity on imported Chinese panels and inverters because they were cheaper and domestic manufacturers could not compete. When policy later pushed localisation through duties and the Approved List of Modules and Manufacturers (ALMM), module manufacturing expanded—but cell dependency persisted.

Now, with ALMM List-II mandating domestic sourcing of cells from 2026, the gap is visible: domestic cell capacity remains a fraction of module capacity. Batteries appear to be at the beginning of the same curve.

The pattern becomes easier to see when placed side by side.

The builders

Over the past five years, a new cohort of founders—largely scientists emerging from institutions such as IIT Madras, IIT Bombay, IISc, and NCL—has begun building battery technology companies from first principles.

Incubators such as IIT Madras, Venture Centre Pune, and Social Alpha have enabled this shift, providing early capital and infrastructure to move ideas from lab to prototype.

Some companies, including Rechargion, Off Grid Energy Labs, Indi Energy, and Sthyr Energy, are working on alternative chemistries such as sodium and zinc. Others, like e-TRNL Energy and Triolt Energy, are rethinking cell architecture to improve charging speeds and safety. Volt14, meanwhile, is focused on anode materials.

In most cases, the company is a continuation of the founder’s research. Early grants and angel capital are often enough to build a prototype and secure basic certification.

What comes next is where the system begins to fray.

Across companies, the constraints are strikingly similar:

● Moving from prototype to pilot requires ₹50–70 crore, well before revenue or validation.

● Manufacturing consistency—moving from a lab cell to thousands of identical units—is a non-trivial leap.

● OEM qualification cycles can run for up to two years, with no guaranteed orders at the end.

● And all the while, the underlying chemistry can shift, sometimes dramatically, altering the economics midstream.

● These are not isolated risks. They compound.

Volt14’s journey offers a window into what navigating this looks like in practice.

Founded in 2018 by Animesh Kumar Jha, a materials scientist from the Hong Kong University of Science and Technology, the company set out to build silicon anode materials for battery cells. It raised a seed round of about $1 million in 2019—and then, over the next five years, raised only about as much again.

In that time, the company focused on building relationships with cell manufacturers. Because its product could only be validated inside a functioning cell, the team had to assemble cells manually in the lab and supply them for testing.

In May 2025, Volt14 raised a pre-Series A round of $1.87 million. The immediate goal is modest: build a small facility to meet early demand. Beyond that lies a pilot line, and then, if all goes well, commercial scale.

Log9 Materials illustrates how fragile that journey can be even at a later stage.

Founded in 2015 at IIT Roorkee, Log9 raised over $70 million and built a pilot manufacturing line around lithium-titanate (LTO) chemistry. But falling lithium iron phosphate (LFP) prices eroded its cost advantage. The company was forced into multiple pivots—importing cells, shifting to an EV leasing model, and exploring the sale of its manufacturing line.

As Nashim Akhtar, who led new initiatives at Log9, puts it: “What’s missing are long-term offtake commitments or demand-side guarantees. Without them, startups remain stuck between pilots and scale.”

What’s missing are long-term offtake commitments or demand-side guarantees. Without them, startups remain stuck between pilots and scale.

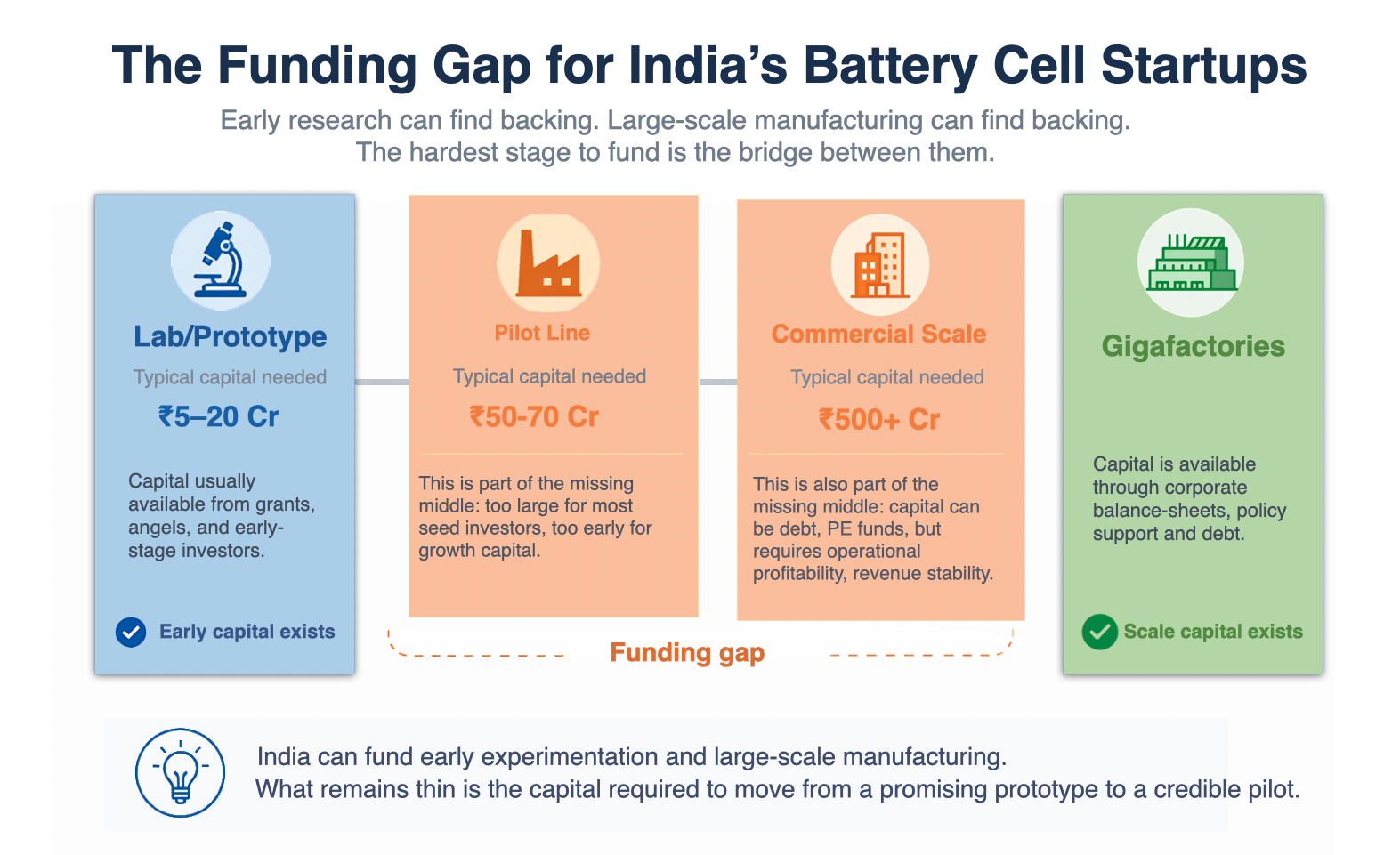

The missing middle

The shape of this gap becomes clearer when you map the capital stack.

The constraint is not the absence of capital. It is the absence of the right kind of capital at the right stages.

At the earliest stage, funding exists. Seed investors such as Speciale Invest and Ankur Capital are backing founders from lab to prototype.

At the other end, capital for large-scale manufacturing is also available. Gigafactories are being financed through corporate balance sheets, policy support, and debt.

India is willing to fund manufacturing scale. It is not yet set up to fund technological risk.

What is missing is the bridge between the two.

The first gap appears at the pilot stage. Moving from prototype to pilot-scale production requires ₹50–70 crore. This is enough to produce cells for testing, but not enough to establish demand. At this point, the bet is largely on the founding team—and most Series A investors require more evidence than that.

The second gap is larger. Scaling from pilot to commercial production (1–5 GWh) requires upwards of ₹500 crore. That level of capital typically comes from private equity or public markets—both of which require stability, visibility, and a path to profitability. A company emerging from the pilot stage has none of these.

This creates a compounding problem. Without growth capital, early-stage investors hesitate. Without early capital, fewer pilots get built. Without pilots, the case for scale never materialises.

One possible bridge is the strategic investor—an incumbent battery or automotive company willing to take a minority stake and offer OEM access in exchange for future technology optionality.

But here, too, the incentives are misaligned.

India’s incumbents are strong in lead-acid batteries, but lithium-ion is not an incremental shift. The overlap in manufacturing processes, materials, and engineering is limited. At the same time, rapid changes in cell chemistry make large capital commitments risky.

The result is caution. Most strategic investments remain exploratory, stopping short of the scale required to meaningfully alter outcomes.

Conclusion

The companies building gigafactories will eventually have to answer a basic question: where will their cell technology come from?

For now, foreign licensing works. But that model may become harder to sustain as geopolitics shifts, licensing costs rise, and policy pushes for deeper localisation.

The government is already signalling direction. India Battery Vision 2047 is being discussed as a roadmap for building a domestic battery supply chain, much like ALMM did for solar.

When that pressure builds, local technology will begin to matter more. The startups that survive long enough to reach demonstration scale will be relevant. Those that run out of capital in the middle will not.

What is emerging is a structural pattern. India is willing to fund manufacturing scale. It is not yet set up to fund technological risk in manufacturing.

Until that changes, the outcome is predictable. Technology will be imported. Domestic players will assemble, optimise, and scale—but not own the core intellectual property.

The factories will be built. The formulas may still come from elsewhere.

Join the conversation

Bharti Krishnan

Founder | Finetrain

Bharti Krishnan, CFA, is the founder of Finetrain, where she works with climate startups on raising equity, debt, and grants. Her work sits at the intersection of finance and climate tech across energy, water, and materials. She spends most of her time meeting founders and helping them think through capital decisions.

Mridu Jhangiani

Founder | Terrarium

Mridu leads Terrarium, a non-profit, volunteer-led community accelerating the adoption of next-gen materials. A Product Design graduate from NID Ahmedabad and currently an MSc candidate at Columbia University, Mridu bridges her design background with her experience in the startup ecosystem to help climate technologies reach scale.

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Loading comments...

More by Bharti Krishnan

Readers also liked

·Economy, Policy & Society

The Quiet Drift Toward Precarity

What the rise of contract labour reveals about the health of India’s factories — and the future of India Inc.

VK

Vineet Kaul

HR Advisor and Mentor

The Quiet Drift Toward Precarity

What the rise of contract labour reveals about the health of India’s factories — and the future of India Inc.

HR Advisor and Mentor

·Leadership & Organisation

Creating Ethical Leaders: Will management education rethink its role?

Two factors are causing a rethink on value systems: environmental degradation and shifts in political power that reflect the voice of the disenfranchised. This new thinking will have to come from new coalitions of social thinkers, practitioners, academics, politicians and corporates

AR

Ajit Rangnekar

Director General of Research and Innovation Circle of Hyderabad | Telangana Government

Creating Ethical Leaders: Will management education rethink its role?

Two factors are causing a rethink on value systems: environmental degradation and shifts in political power that reflect the voice of the disenfranchised. This new thinking will have to come from new coalitions of social thinkers, practitioners, academics, politicians and corporates

Director General of Research and Innovation Circle of Hyderabad | Telangana Government

·Economy, Policy & Society

Will technology destroy democracy?

Job destruction, fake news, polarisation. Rapid advances in technology are blamed for these. Is that claim justified? Are other factors at play? Who will regulate technology?

AM

Arun Maira

Former Chairman, BCG India | Member, Planning Commission

Will technology destroy democracy?

Job destruction, fake news, polarisation. Rapid advances in technology are blamed for these. Is that claim justified? Are other factors at play? Who will regulate technology?

Former Chairman, BCG India | Member, Planning Commission

Explore more

Dive into other themes from our network.